The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Bread Financial (NYSE:BFH) and the rest of the credit card stocks fared in Q2.

Credit card companies facilitate electronic payments and extend revolving credit to consumers. Growth comes from increasing digital payment adoption, cross-border transaction growth, and value-added services for cardholders and merchants. Challenges include regulatory scrutiny of fees and practices, competition from alternative payment methods, and potential credit losses during economic downturns.

The 6 credit card stocks we track reported a strong Q2. As a group, revenues were in line with analysts’ consensus estimates.

In light of this news, share prices of the companies have held steady as they are up 5% on average since the latest earnings results.

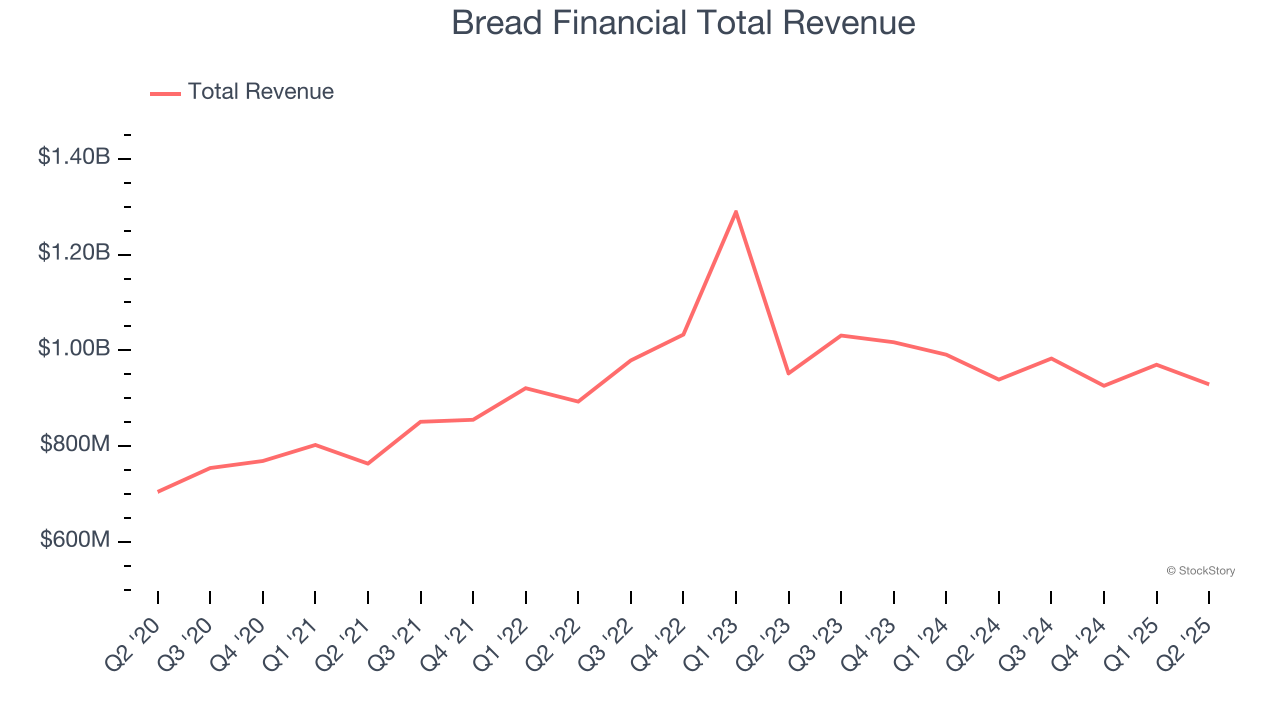

Best Q2: Bread Financial (NYSE:BFH)

Formerly known as Alliance Data Systems until its 2022 rebranding, Bread Financial (NYSE:BFH) provides credit cards, installment loans, and savings products to consumers while powering branded payment solutions for retailers and merchants.

Bread Financial reported revenues of $929 million, down 1.1% year on year. This print fell short of analysts’ expectations by 0.6%, but it was still a very strong quarter for the company with a beat of analysts’ EPS estimates.

Interestingly, the stock is up 4.3% since reporting and currently trades at $66.98.

Is now the time to buy Bread Financial? Access our full analysis of the earnings results here, it’s free.

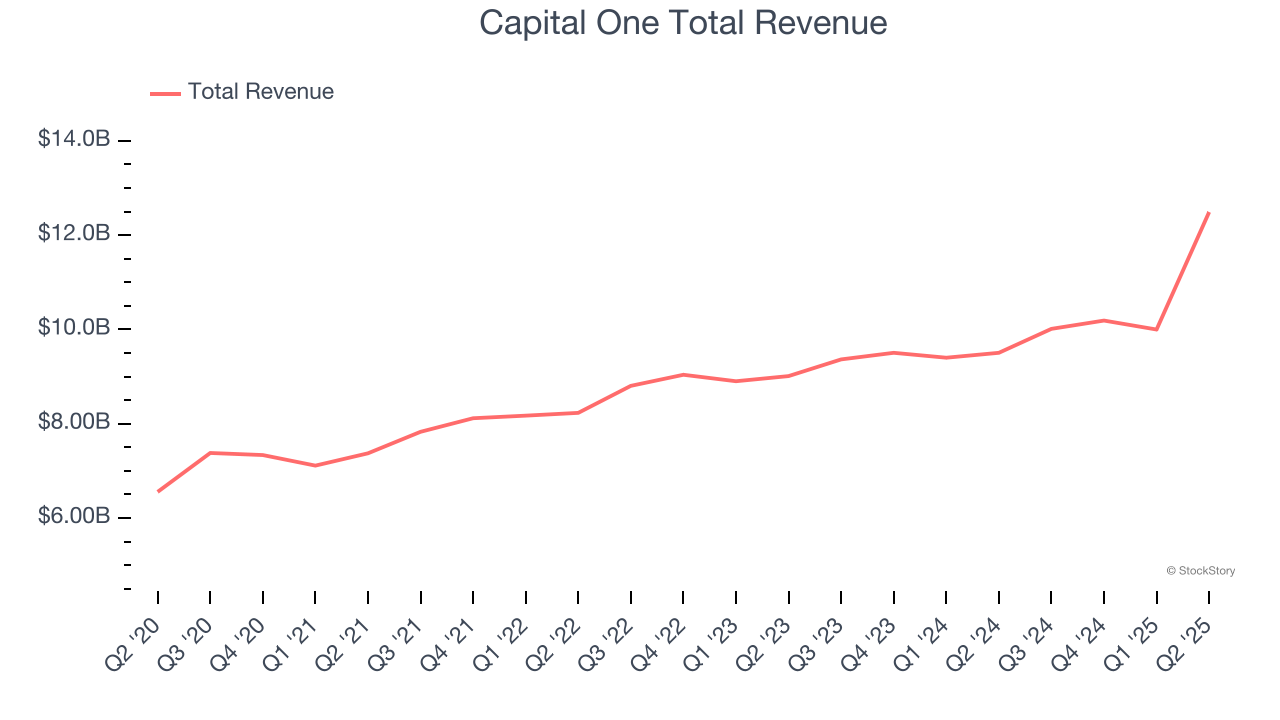

Capital One (NYSE:COF)

Starting as a credit card company in 1988 before expanding into a full-service bank, Capital One (NYSE:COF) is a financial services company that offers credit cards, auto loans, banking services, and commercial lending to consumers and businesses.

Capital One reported revenues of $12.49 billion, up 31.4% year on year, falling short of analysts’ expectations by 1.2%. However, the business still had a strong quarter with a beat of analysts’ EPS and net interest margin estimates.

Capital One pulled off the fastest revenue growth among its peers. The market seems content with the results as the stock is up 4% since reporting. It currently trades at $225.90.

Is now the time to buy Capital One? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: American Express (NYSE:AXP)

Recognizable by its iconic green logo and the slogan "Don't leave home without it," American Express (NYSE:AXP) is a global payments company that issues credit and charge cards, processes merchant transactions, and offers travel and lifestyle benefits to consumers and businesses.

American Express reported revenues of $13.24 billion, up 9.4% year on year, in line with analysts’ expectations. Still, it was a satisfactory quarter as it posted a narrow beat of analysts’ transaction volumes estimates.

Interestingly, the stock is up 4.7% since the results and currently trades at $330.50.

Read our full analysis of American Express’s results here.

Synchrony Financial (NYSE:SYF)

Powering over 73 million active accounts and partnerships with major brands like Amazon, PayPal, and Lowe's, Synchrony Financial (NYSE:SYF) provides credit cards, installment loans, and banking products through partnerships with retailers, healthcare providers, and digital platforms.

Synchrony Financial reported revenues of $3.65 billion, down 1.8% year on year. This number missed analysts’ expectations by 1.3%. In spite of that, it was a strong quarter as it put up a beat of analysts’ EPS estimates and an impressive beat of analysts’ net interest margin estimates.

Synchrony Financial had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is up 11.2% since reporting and currently trades at $77.26.

Read our full, actionable report on Synchrony Financial here, it’s free.

Visa (NYSE:V)

Processing over 829 million transactions daily and connecting billions of cards to 150 million merchant locations worldwide, Visa (NYSE:V) operates one of the world's largest electronic payments networks, facilitating secure money movement across more than 200 countries through its VisaNet processing platform.

Visa reported revenues of $10.17 billion, up 14.3% year on year. This result surpassed analysts’ expectations by 3.3%. Overall, it was a strong quarter as it also produced a solid beat of analysts’ transaction volumes estimates and an impressive beat of analysts’ EBITDA estimates.

Visa pulled off the biggest analyst estimates beat among its peers. The stock is flat since reporting and currently trades at $350.78.

Read our full, actionable report on Visa here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.