Regional banking company Banner Corporation (NASDAQ:BANR) fell short of the market’s revenue expectations in Q2 CY2025, but sales rose 8.3% year on year to $162.2 million. Its GAAP profit of $1.31 per share was 0.8% below analysts’ consensus estimates.

Is now the time to buy Banner Bank? Find out by accessing our full research report, it’s free.

Banner Bank (BANR) Q2 CY2025 Highlights:

- Net Interest Income: $144.4 million vs analyst estimates of $146.2 million (8.9% year-on-year growth, 1.2% miss)

- Net Interest Margin: 3.9% vs analyst estimates of 4% (22 basis point year-on-year increase, 3.8 bps miss)

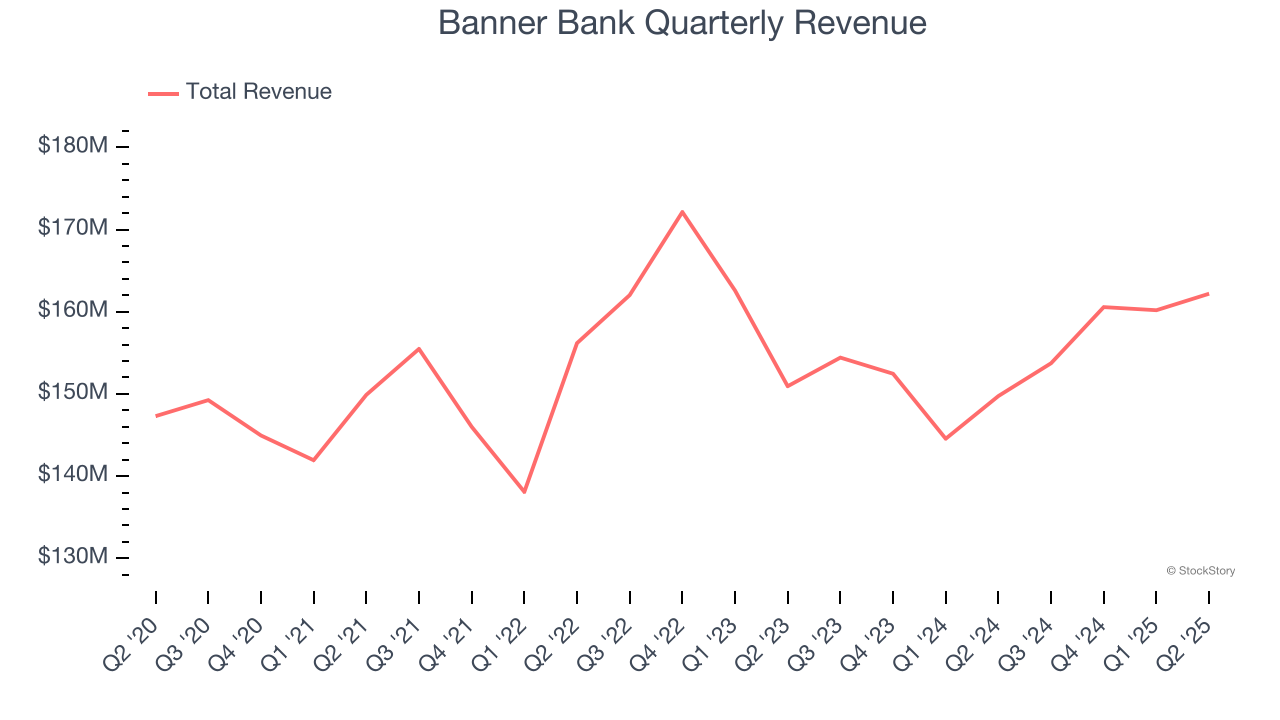

- Revenue: $162.2 million vs analyst estimates of $163.7 million (8.3% year-on-year growth, 0.9% miss)

- Efficiency Ratio: 62.5% vs analyst estimates of 61.1% (1.4 percentage point miss)

- EPS (GAAP): $1.31 vs analyst expectations of $1.32 (0.8% miss)

- Market Capitalization: $2.3 billion

“Banner’s second quarter performance highlights the strength of our super community bank strategy, which focuses on building client relationships, preserving a strong funding base, and delivering exceptional service while sustaining a moderate risk profile,” said Mark Grescovich, President and CEO.

Company Overview

Founded in 1890 in Walla Walla, Washington, and evolving through more than a century of economic cycles, Banner Corporation (NASDAQ:BANR) operates Banner Bank, providing commercial banking services, loans, and financial products to individuals and businesses across Washington, Oregon, California, Idaho, and Utah.

Sales Growth

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

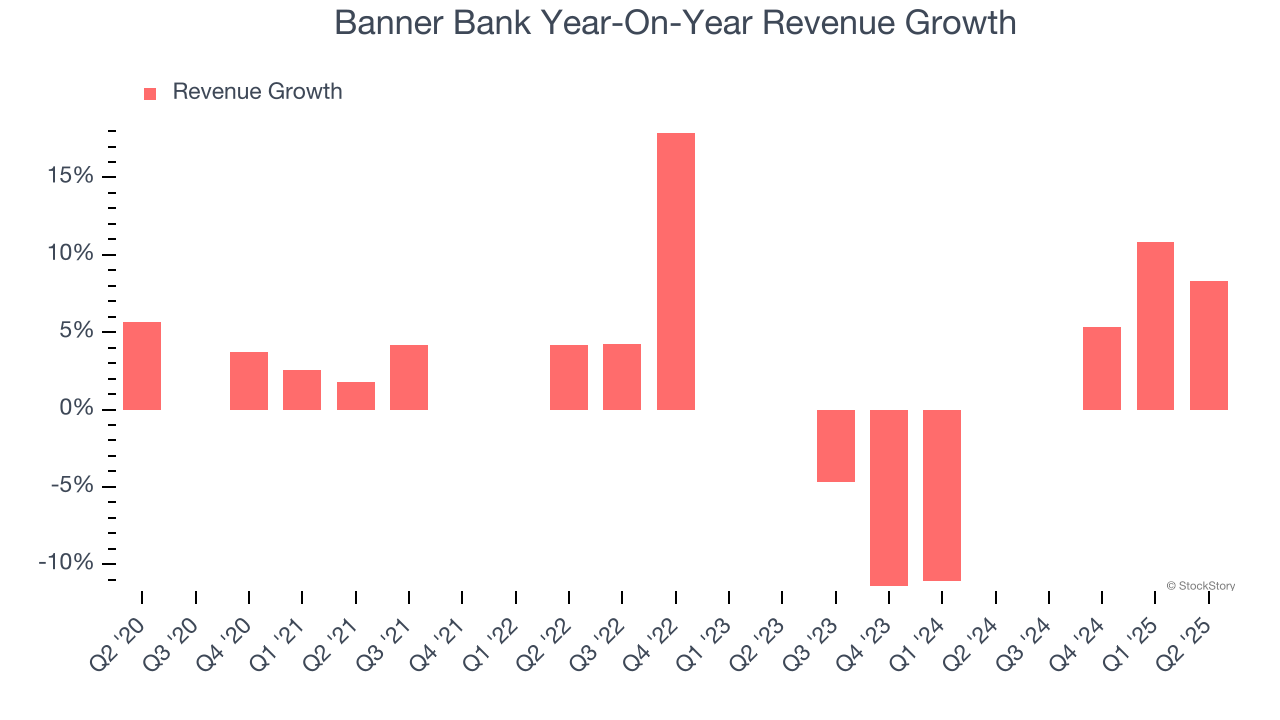

Regrettably, Banner Bank’s revenue grew at a tepid 2.5% compounded annual growth rate over the last five years. This was below our standards and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Banner Bank’s recent performance shows its demand has slowed as its revenue was flat over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Banner Bank’s revenue grew by 8.3% year on year to $162.2 million, missing Wall Street’s estimates.

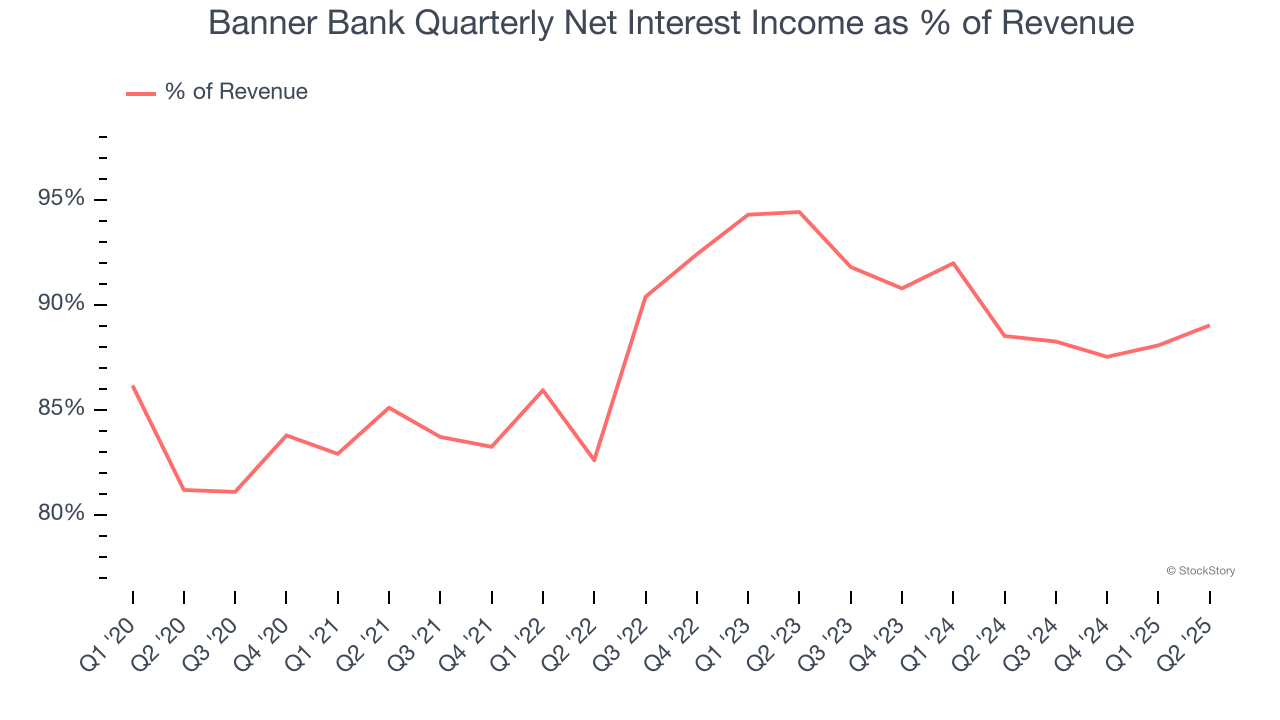

Net interest income made up 87.8% of the company’s total revenue during the last five years, meaning Banner Bank barely relies on non-interest income to drive its overall growth.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

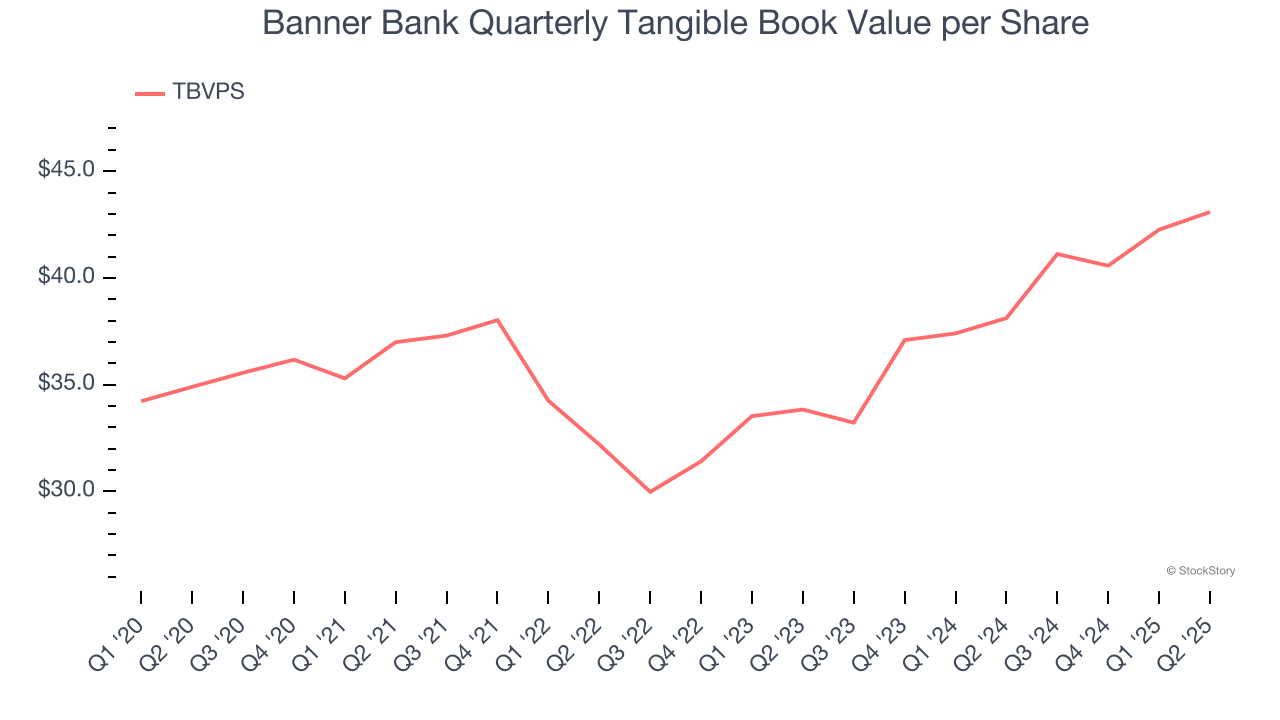

Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Banner Bank’s TBVPS grew at a mediocre 4.3% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 12.9% annually over the last two years from $33.83 to $43.09 per share.

Over the next 12 months, Consensus estimates call for Banner Bank’s TBVPS to grow by 10.5% to $47.61, solid growth rate.

Key Takeaways from Banner Bank’s Q2 Results

We struggled to find many positives in these results as Banner missed Wall Street’s estimates across all key metrics. Overall, this was a weaker quarter. The stock remained flat at $66.83 immediately following the results.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.